Cases in Japan

![]()

![]()

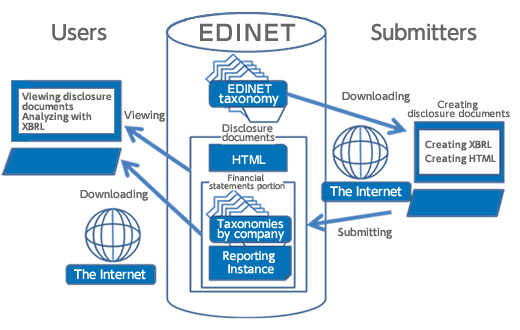

EDINET stands for ‘Electronic Disclosure for Investors’ NETwork’, which is an electronic disclosure system of securities reports based on the requirement of Financial Instrument and Exchange Law. EDINET was developed to reduce the burden of office work of companies, to realize fair and quick access to companies’ data by investors, and to improve efficiency of securities market by changing the procedure of submission and public inspection from paper to electronic data, in terms of disclosure documents such as financial statements and securities registration statements. Specifically, submitters of securities reports are to submit them through the internet addressed to regional finance bureaus and others. Submitted disclosure information is accessible freely by anyone at anywhere through the internet.

Figure 1 about EDINET

Introduction of XBRL

EDINET system started its operation in 2001 and gradually expanding its objects year by year. In March 2008, ‘New EDINET’ started its operation employing XBRL in the area of financial statements in companies’ security reports. In New EDINET, the data of disclosure documents are not only for viewing but they can be utilized for also downloading and processing. The XBRL data can be installed into wide range of applications regardless of computer operating environment, therefore it makes many investors to process and analyze financial information efficiently.

Submitters of disclosure documents were requested to submit disclosure documents in XBRL format from April 1, 2008.

The applied range of XBRL

In New EDINET, among the submitted financial statements listed in securities registration statements, semiannual securities reports, quarterly securities reports, XBRL is to be used for consolidated financial statements (consolidated balance sheets, consolidated profit and loss statements, consolidated statements of changes in net assets and consolidated cash flow statements) and non-consolidated financial statements (balance sheets, profit and loss statements, statements of changes in net assets) except noted items and schedule.

The other areas of statements should be made in HTML.

Companies making consolidated financial statements based on US standards should make consolidated financial statements in HTML as before, and should make non-consolidated financial statements in XBRL.

| From 2008 | From 2013 | |

| Securities Registration Statement |

○ (Covers only the main table) |

○ (Covers the entire disclosure documents) |

| Financial Statement | ○ (Covers only the main table) |

○ (Covers the entire disclosure documents) |

| Quarterly Report | ○ (Covers only the main table) |

○ (Covers the entire disclosure documents) |

| Semi-annual Report | ○ (Covers only the main table) |

○ (Covers the entire disclosure documents) |

| Current Report | ○ | |

| Shelf Registration Statement | ○ | |

| Supplementary Documents to the Shelf Registration Statement |

○ | |

| Report on the Issuer’s Own Stock Repurchase | ○ | |

| Registration Statement of Tender Offer | ○ | |

| Position Statement | ○ | |

| Registration Statement of Withdrawal of Tender Offer |

○ | |

| Tender Offer Report | ○ | |

| Tender Offeror's Answer | ○ | |

| Substantial Shareholding Report | ○ | |

| Internal Control Report | ○ |

Tagging (Comprehensive Tags and Detailed Tags)

There are two ways of tagging on EDINET which enable us to extract information in units of tagging.

□Comprehensive Tag: Used for enclosing whole information including sentences and tables.

□ Detailed Tag: Used for individual item in a unit such as strings, sentences, amount and numeric values.

For example, in a financial statement, comprehensive tags are used for enclosing the entire information in a report, generally per section. Detailed tags are used for the following information:

| ● The cover (company name, company code and accounting period, etc.) |

| ● The history of principal management indexes |

| ● The situation of major stockholders |

| ● The main table of a financial statement (*) |

| ● A part of notes related to balance sheets (*) |

| ● A part of notes related to profit and loss statements (*) |

| ● Segment information (*) |

| * Detailed tags are required in Japanese standards. In IFRS, they are optional. In U.S., they are not the target of detailed tags. |

Reference: "EDINET概要書(Introduction to EDINET)","EDINETタクソノミの概要説明(Beginner’s Guide to EDINET Taxonomy)"

![]()

![]()

![]()